Buying car insurance doesn’t have to be complicated or expensive. Yet, millions of Indians overpay thousands of rupees every year simply because they don’t understand how car insurance works or believe the process is too complex to handle themselves.

Here’s a shocking truth: In our research, we found that the exact same insurance policy costing ₹61,503 when bought online was quoted at ₹1,05,000 by a car dealer—that’s a difference of ₹43,497! Similarly, for a 4-year-old Hyundai Venue, the dealer quoted ₹18,000 while the online price was just ₹11,238—a savings of nearly ₹7,000 for a 10-minute online process.

This comprehensive guide will demystify car insurance, explain every term in simple language, and show you exactly how to buy the right coverage while saving significant money. Whether you’re buying insurance for a brand-new car or renewing an existing policy, this guide has everything you need.

Understanding the Basics: Why Car Insurance Matters

Before diving into the technical details, let’s understand why car insurance is essential. In India, third-party insurance is mandatory by law. If you’re caught driving without it, you’ll face a challan (fine). However, first-party or comprehensive insurance, while not legally required, protects your own vehicle from damage.

The reality is that 90% of Indians purchase or renew their insurance through dealers, agencies, or nearby shops. Why? Two main reasons:

- Lack of knowledge about insurance terms and processes

- Fear of missing important coverage that could cause claim rejection later

The good news? Car insurance is straightforward enough that even a fifth-grade student can understand it. Once you grasp the basics, you can confidently purchase insurance online in minutes, saving thousands in the process.

Third-Party vs First-Party Insurance: What’s the Difference?

Understanding the distinction between third-party and first-party insurance is fundamental to making smart insurance decisions.

What is Third-Party Insurance?

Imagine you’re driving your car on a busy road. Another vehicle approaches from the opposite direction, and unfortunately, an accident occurs—and it’s your fault. Both cars sustain damage.

The “third party” refers to any other vehicle or person on the road besides you (the first party) and your insurance company (the second party).

If you only have third-party insurance and the accident is your fault, your insurance company will compensate the other car owner for all damages. This is why third-party insurance is mandatory in India—it ensures that if you cause an accident, the innocent party doesn’t suffer financially.

Key Point: Even if the other car has its own insurance, your insurance company pays because you were at fault.

What is First-Party (Comprehensive) Insurance?

Now, let’s say you have first-party insurance (also called comprehensive insurance) and you’re at fault in an accident. In this scenario, your insurance company will pay for:

- Damage to the other person’s car (third-party coverage)

- Damage to your own car (first-party coverage)

The Cost Difference: If third-party insurance costs ₹100, comprehensive insurance typically costs around ₹130—a relatively small increase for complete protection.

The Hidden Catch: Why Comprehensive Insurance Only Pays 50%

Here’s where many people get confused. Even with comprehensive insurance, you won’t receive 100% coverage for all damages. Let me explain:

If your car meets with an accident causing ₹50,000 worth of damage (₹25,000 to each vehicle), your insurance company won’t pay the full amount.

The Depreciation Rule:

- Plastic parts damage worth ₹10,000 → You get only ₹5,000 (50%)

- Glass/windshield damage worth ₹20,000 → You get only ₹10,000 (50%)

- Rubber parts/tyres damage → You get only 50% coverage

For most body parts, you’ll receive only 50% reimbursement, meaning you must pay the remaining 50% from your pocket. This is where zero-depreciation insurance becomes crucial.

Zero-Depreciation Insurance: The Game-Changer

Zero-depreciation insurance (also called “zero-dep” or “bumper-to-bumper” insurance) is the single most important add-on you should purchase.

How Zero-Dep Works

When you have zero-depreciation coverage and your car meets with an accident:

- You take the damaged car to the authorized agency/workshop

- Document the accident immediately with photos or video (this serves as crucial evidence)

- The agency handles the repairs

- Your insurance company reimburses 100% of the costs—not 50%

What’s Covered 100%:

- Plastic body parts

- Glass and windshield

- Rubber components

- Tyres

- Metal body panels

Important Clarification: You cannot purchase zero-depreciation insurance with only third-party coverage. It’s an add-on that requires comprehensive (first-party) insurance as the base policy.

The Small File Charges

You might hear that agencies charge ₹1,000-₹1,500 as “file charges” even with zero-dep insurance. This is normal and significantly cheaper than paying 50% of repair costs yourself.

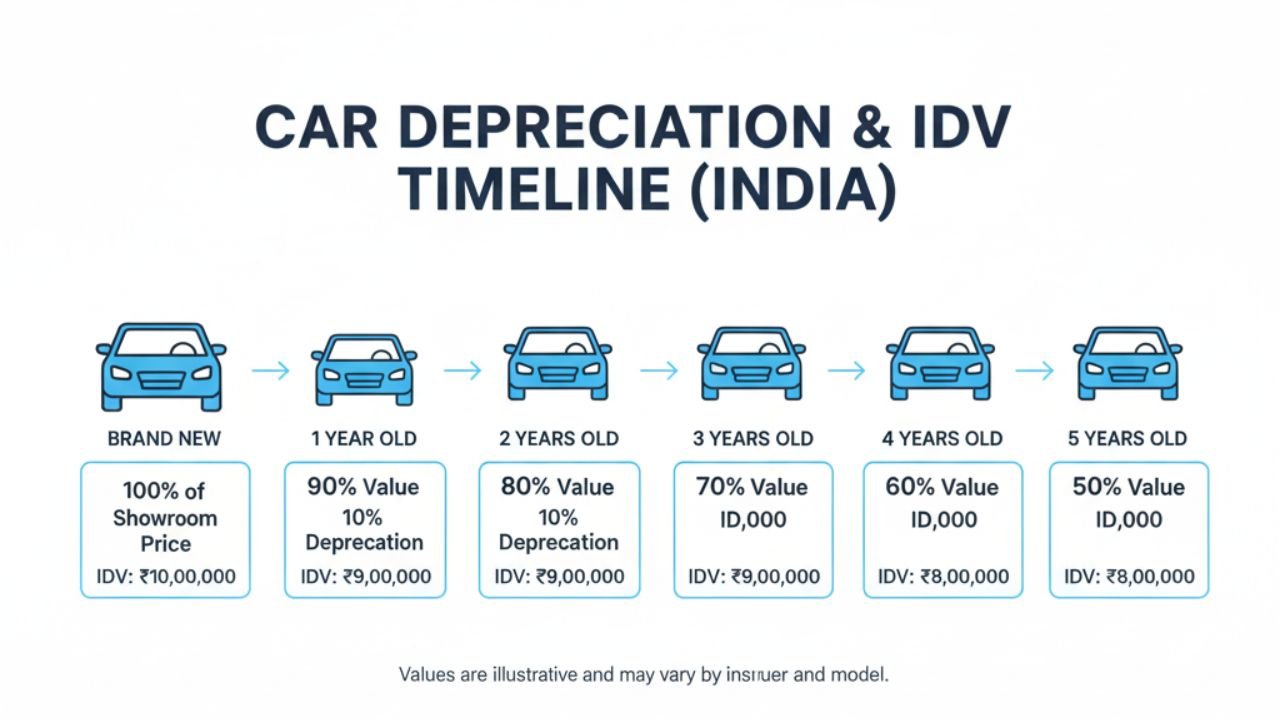

Understanding IDV: Insured Declared Value

IDV (Insured Declared Value) represents the current market value of your car at the time of insurance renewal. It’s crucial because this is the maximum amount you’ll receive in case of total loss or theft.

How IDV is Calculated

For Brand-New Cars: When insuring a car for the first time (straight from the showroom), the IDV is calculated as:

- Ex-showroom price minus 5%

Example: If your car’s ex-showroom price is ₹20,99,000:

- 5% depreciation = ₹1,04,950

- IDV = ₹19,94,050

Note: Insurance is always calculated on the ex-showroom price, NOT the on-road price (which includes insurance and RTO charges).

IDV Depreciation Schedule for Older Cars

|

Car Age

|

Depreciation

|

IDV Calculation

|

|---|---|---|

|

0-6 months

|

5%

|

95% of ex-showroom

|

|

6 months – 1 year

|

15%

|

85% of ex-showroom

|

|

1-2 years

|

20%

|

80% of ex-showroom

|

|

2-3 years

|

30%

|

70% of ex-showroom

|

|

3-4 years

|

40%

|

60% of ex-showroom

|

|

4-5 years

|

50%

|

50% of ex-showroom

|

|

5+ years

|

Your choice

|

Below 50% acceptable

|

Real Example: A car purchased for ₹10 lakhs that’s now 4 years old would have an IDV of approximately ₹5 lakhs (50% depreciation).

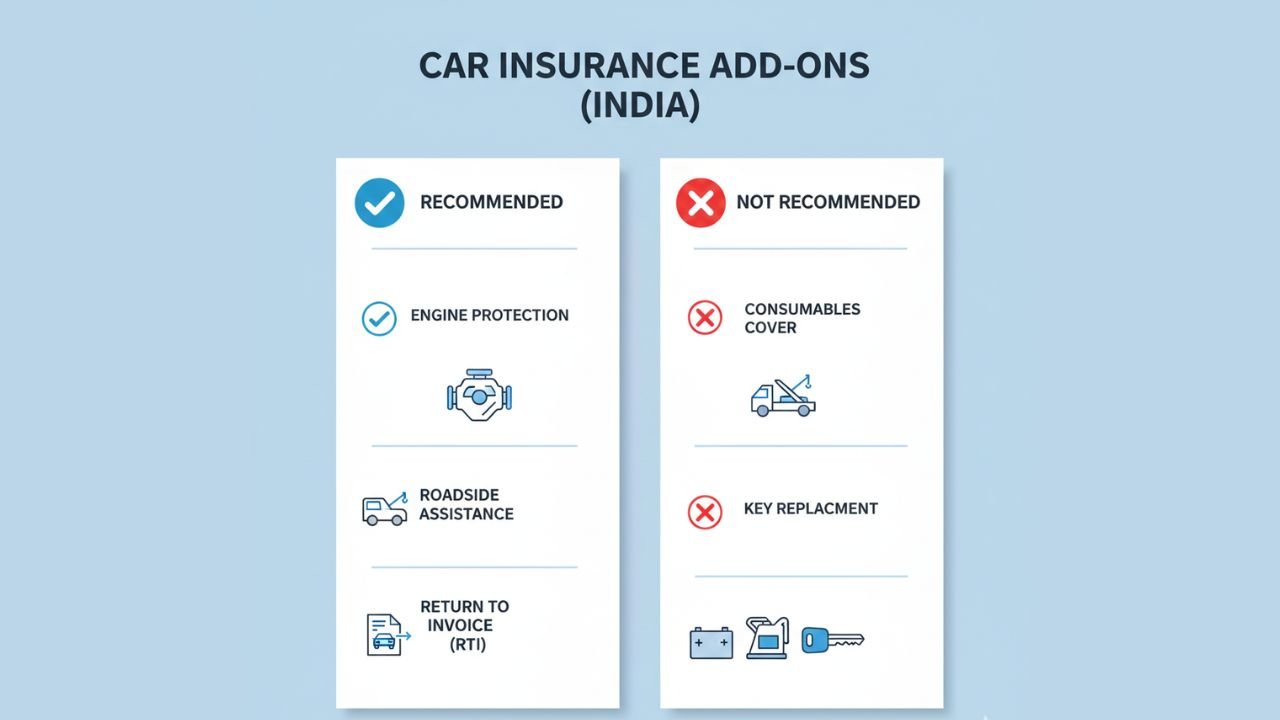

Essential Add-On Covers You Should Consider

Beyond basic comprehensive and zero-depreciation coverage, several add-ons can enhance your protection:

1. Engine Protection Cover (MANDATORY)

- Why it’s critical: Zero-depreciation covers body parts but NOT engine damage. The engine is your car’s most expensive component and lifeline.

- When you need it: If your car suffers a head-on collision or water logging that damages the engine, this cover ensures 100% reimbursement.

- Don’t skip this! Many people mistakenly believe zero-dep covers everything—it doesn’t.

2. Consumables Cover (HIGHLY RECOMMENDED)

- What it covers: Nuts, bolts, grease, engine oil, brake fluid, and other items “consumed” during repairs.

- Why important: These small items add up during major repairs, and without this cover, you’ll pay for them separately.

3. Roadside Assistance (RECOMMENDED)

What it provides: 24×7 emergency support including:

- Towing services

- Battery jump-start

- Flat tyre change

- Fuel delivery

Cost: Typically ₹500-₹700 extra Verdict: Worth it if you frequently travel alone or on highways

4. Return to Invoice (RTI) Cover (SITUATIONAL)

What it does: If your car is stolen or totaled, RTI pays the original invoice price instead of the depreciated IDV.

Example:

- You bought a car for ₹10 lakhs 4 years ago

- Current IDV: ₹5 lakhs

- Without RTI: You get ₹5 lakhs

- With RTI: You get ₹10 lakhs

Best for: New cars (1-3 years old) where the gap between IDV and invoice price is significant

5. Key and Lock Replacement (OPTIONAL)

Covers costs if you lose your car keys or they’re stolen. Skip if you’re careful with keys.

6. Tyre Protector (NOT RECOMMENDED)

Separate tyre damage coverage. Generally not worth it since zero-dep already covers tyre damage from accidents.

7. Loss of Personal Belongings (NOT RECOMMENDED)

Covers items stolen from your car during an accident. Creates documentation headaches—skip it.

8. Daily Allowance (NOT RECOMMENDED)

Provides Uber vouchers (₹200-₹250/day) while your car is being repaired. Nice to have but not essential.

Real-Life Cost Comparison: Dealer vs Online

Let’s examine actual examples that demonstrate massive savings:

Example 1: Brand-New XUV AX7 (₹21 Lakhs)

Dealer Quote:

- Comprehensive insurance: ₹1,05,000

- Negotiated best price: ₹95,000

Online Quote (ICICI Lombard):

- Same coverage with ALL add-ons: ₹61,503

- Savings: ₹33,497 to ₹43,497

Example 2: 4-Year-Old Hyundai Venue (IDV ₹5 Lakhs)

Dealer Quote:

- Comprehensive + zero-dep + engine protection + consumables + roadside assistance + personal accident cover: ₹18,000

Online Quote:

- Same coverage (minus roadside assistance and personal accident): ₹11,238

- Even adding those two missing covers (₹699 + ₹675 = ₹1,374): Total ₹12,612

- Savings: ₹5,388

The Reality: Dealers charge ₹5,000-₹7,000 extra for a 10-minute online process you can do yourself!

Step-by-Step: How to Buy Car Insurance Online

For Brand-New Cars (No Registration Number Yet)

- Visit insurance website (ICICI, HDFC, Acko, PolicyBazaar, etc.)

- Click “Brand New Car” option (don’t enter registration number)

- Fill in car details: Model, variant, ex-showroom price

- Select IDV: Automatically calculated as 95% of ex-showroom

- Choose policy type: 1-year comprehensive + 3-year third-party (mandatory for new cars)

- Add covers: Zero-dep, engine protection, consumables, RTI, roadside assistance

- Enter engine and chassis number (from your car documents)

- Make payment and receive policy instantly

For Insurance Renewal (Existing Cars)

- Enter registration number on insurance website

- Verify car details auto-populated

- Set IDV based on car’s age (use depreciation table above)

- Select add-ons you want

- Check No Claim Bonus (NCB) if applicable

- Pay and download policy

Time Required: 5-10 minutes Documents Needed: Registration certificate, previous policy (for renewal), engine/chassis number (for new cars)

Common Mistakes to Avoid

Mistake 1: Skipping Zero-Depreciation

Saving ₹2,000-₹3,000 now but paying lakhs later in partial claim settlements.

Mistake 2: Not Taking Engine Protection

Assuming zero-dep covers everything. Engine damage claims can exceed ₹2-3 lakhs.

Mistake 3: Overpaying at Dealerships

Paying 30-50% more for the exact same policy out of convenience or fear.

Mistake 4: Wrong IDV Declaration

Declaring too low IDV to save premium but receiving inadequate compensation in total loss.

Mistake 5: Not Documenting Accidents

Failing to photograph accident scenes immediately, leading to claim disputes.

Frequently Asked Questions

Q: Can I buy insurance from any company, or must I use the dealer’s recommendation? A: You have complete freedom to choose any insurance provider—ICICI, HDFC, Acko, Bajaj Allianz, or any IRDAI-approved company. Dealers cannot force you.

Q: Is online insurance valid and legitimate? A: Absolutely! Online policies are 100% legal and identical to offline policies. The only difference is price and convenience.

Q: What if I make a mistake while filling the online form? A: Most platforms allow corrections before payment. After purchase, you can request endorsements for minor changes.

Q: Will claims be rejected if I buy online? A: No! Claim settlement depends on policy terms, not purchase channel. Online buyers get identical claim support.

Q: How do I get help if I don’t understand the process? A: Watch tutorial videos, read guides like this one, or ask a tech-savvy friend to help you once. After that, you’ll do it independently.

Final Verdict: Take Control of Your Car Insurance

The car insurance process in India is deliberately made to seem complex, but it’s actually straightforward. By understanding:

- The difference between third-party and comprehensive coverage

- How IDV calculation works

- Which add-ons are essential (zero-dep, engine protection, consumables)

- The simple online purchase process

You can save ₹5,000-₹40,000+ every year while getting equal or better coverage than dealer-quoted policies.

Action Steps:

- Never accept the first dealer quote

- Always get online quotes for comparison

- Include zero-depreciation, engine protection, and consumables

- Consider RTI for cars less than 3 years old

- Spend 10 minutes learning the process—it’ll save you lakhs over your car’s lifetime

Remember, insurance companies and dealers profit from your lack of knowledge. Educate yourself, take control, and make smart financial decisions. Your wallet will thank you!

Ready to save on your next car insurance? Visit platforms like PolicyBazaar, Acko, or directly go to ICICI Lombard, HDFC Ergo, or Bajaj Allianz websites. Enter your car details, compare quotes, and purchase in minutes. The process is simpler than ordering food online—and the savings are substantial!

Have questions about car insurance? Drop them in the comments below, and don’t forget to share this guide with friends and family who might be overpaying for their car insurance!

Leave a Comment